Now you’re playing with power – 21st century investing with Robo Financial Advisors

The robot uprising has been quieter than expected. In fact, few even heard it coming, let a lone in the form of Robo Financial Advisors.

In recent years the unemotional, efficient analyses of so-called “Robo-Advisers” has pushed to the forefront of investing services. Can the investing acumen of an entity comprised of programming code outperform traditional advisers?

In this article we’ll seek to answer this question through a review of the services offered by robo-advisers. We’ll consider the behavioral finance advantages to this new method and how engaging in this practice illuminates your own risk tolerance. Finally, we’ll review the costs involved and how robo-advisers can accomplish retirement goals.

A restriction on impulse

When you interact with a robo-adviser service you’re plotting a course then engaging autopilot. This has a distinct advantage that’s less evident with traditional investing. When you’ve committed to a set plan upfront you’re far less likely to deviate. Robo-adviser services seem to have the unintended benefit of countering the problems of behavioral finance.

The emerging field of behavioral finance endeavors to explore the notion that you, the investor, are your own worst enemy. In the past traditional economics has been the tool in understanding how and why business, markets and individuals operate as they do. Today this is changing.

Experts have incorporated cognitive and behavioral psychological theory to more clearly understand why rational decision making can so dramatically breakdown. It is these breakdowns that can cause loss of personal wealth and at it’s worst decimate entire markets. Irrational thinking leads to economic problems.

Consider the findings of a paper published by The Research Foundation of CFA Institute Literature Review. The author explains, “one aspect of the discussion about rational and irrational investors that is important to consider is the extent to which professional traders and money managers are subject to the same behavioral biases that are more commonly discussed in the context of individual (typically assumed uninformed) investors.” By removing humans, including yourself, from the process you’re creating a barrier to this problem.

You’re the programmer

Many mistakenly believe that opting for a robo-adviser takes away their financial control entirely. This is untrue.

Many mistakenly believe that opting for a robo-adviser takes away their financial control entirely. This is untrue.

While the robo-adviser will generate a specifically curated portfolio of investments it will do so in response to your risk tolerance. You are driving the major parameters. It is from this point that the robo-adviser will begin working.

It can be argued that this in fact puts more agency in your hands. As you are guided through a series of questions about investment preferences you’ll come to an understanding of your own psychological profile. The result: you’re making decisions without the implicit or explicit influence of an “expert.” Instead of market fads or alluring speculative trades, your plan will be restricted to more pertinent factors…

The primary attributes:

- Age

- Income

- Single/Duel income

- Dependents/No Dependents

- Current savings

- Risk tolerance

The irony is that a robo-adviser will put you in the picture more than a traditional money manager will. There are no commissions or motivations to push certain investment products. The conversation is focused on where you are financially and where you want to go. The questions are answered in private without uncomfortable silences or the influence of needlessly complex marketing materials.

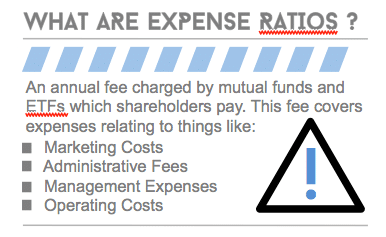

Minimizing expenses

Robo-advisers offer among the lowest fees. The process is streamlined and efficient thereby rooting out costs that erode wealth in the long-term.

The reduced expenses also come from a cost efficient selection of funds. Robo-advisers maximize returns by restricting the suggested mutual funds, ETFs and bonds to those with the lowest expense ratios. The benefit of this practice is most visible over a long-term horizon where the magic of compound growth can amplify wealth. In many cases these annual ETF costs will range from 0.05% to 0.75%. Be cognizant of your exposure to costs. Some annual fees will also apply. These differ from among robo-advisers but you can expect to pay .15% to .75% annually as a service fee.

Retirement in the digital age

Robo-advisers are up to the task of retirement planning because it is a game of consistency and discipline. The automatic rebalancing option offered by many robo-advisers can help achieve the “slow and steady” mentality that is so crucial for long-term investors. Markets will rise and fall but the machines will not respond emotionally even if you do. This is to your benefit.

The algorithms involved in robo-advising are also optimized for tax loss harvesting. This complex practice is simplified with the aid of automation. Those planning their retirement will find enormous value in this cost-cutting measure.

A robo-adviser is an excellent option for any investor. The simplified, low cost approach is perfect for beginners and high net worth clients alike.

For more insights and perspectives on managing the workplace, discover TemPositions’ blog.